Article by Mikolaj Nowakowski

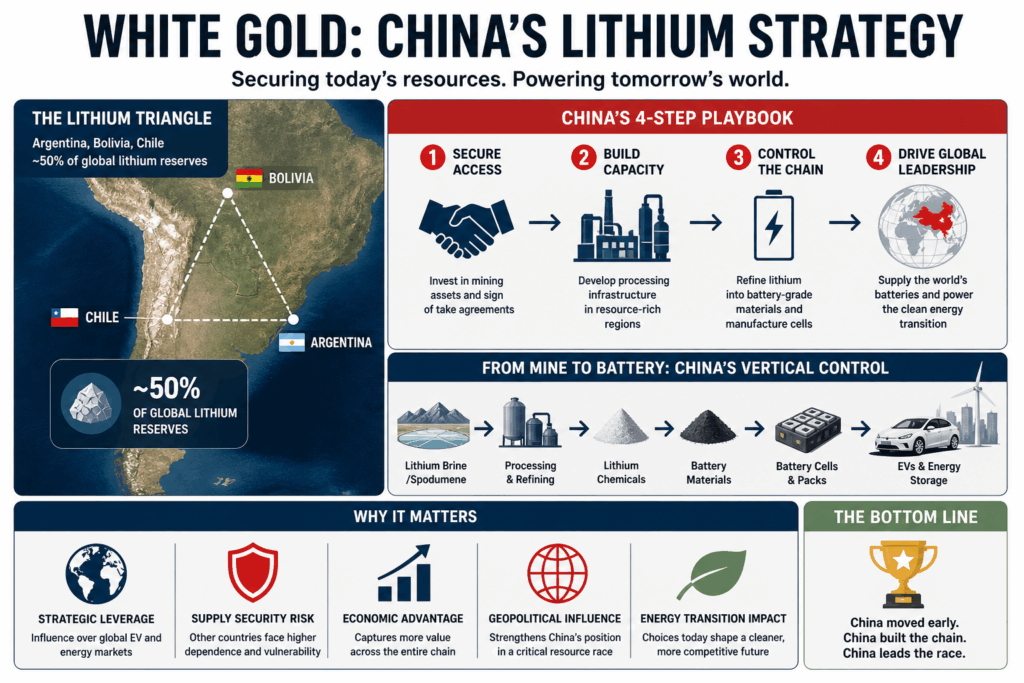

There is a region in South America where Argentina, Bolivia, and Chile meet at an extreme altitude that may turn out to be one of the most strategically important pieces of land on earth. It is commonly known as the Lithium Triangle. Roughly 50% of the world’s identified lithium reserves can be found there, and because the global economy pivots toward electric vehicles and grid-scale energy storage, whoever controls this resource dictates the economic development of numerous countries.

China figured this out early. While Western governments were still debating climate policy frameworks, Chinese companies were signing offtake agreements, acquiring minority stakes in mining operations in the region, and building the processing infrastructure needed to turn raw lithium into battery cells. Slowly, but surely, developing a vertical supply chain. More than a decade later, those actions resulted in a position of extraordinary structural advantage, not just in South America, but across the entire lithium supply chain.

This article is an attempt to explain how that happened, and what it means for all of us.

The Triangle Itself

Lithium is a soft, silvery-white alkali metal that is used in the production of lithium-ion batteries. They power not only EVs but also are used in the grid storage sector, as well as portable electronics. The aforementioned use cases account for roughly 87% of the total demand. So, without lithium, the global energy transition would effectively stall. Moreover, no commercially viable alternative at scale only strengthens the leverage China and others can use. The lithium-ion battery market alone is valued at over $150 billion and is projected to exceed $400 billion by the early 2030s, driven almost entirely by electrification and grid storage buildout. So, how does the region of interest in South America actually look?

The lithium in this area sits in salt flats called salares, vast, blinding white expanses at altitudes above 3,500 meters, where ancient lakes evaporated. The leftover brine is saturated with a mix of lithium, potassium, and magnesium. And the approach of the three countries in question to the extraction of those deposits is strikingly different. Let us start with the most important one – Bolivia. It holds the largest reserves globally, somewhere around 23 million tonnes (circa 20% of global reserves), and has historically kept them under strict state control. The logic was sovereign and totally justifiable. Bolivia is a landlocked country with a colonial history. As a protectorateof Spain for nearly 300 years, it watched its natural resources being extracted by foreign powers with little to no local benefit. Lithium was supposed to be different. The resource Bolivia would develop on its own terms, capturing the value domestically rather than exporting raw ore. There is one catch, however. Building a lithium industry from scratch requires massive amounts of capital expenditure that Bolivia cannot afford, and with the infrastructure that it doesn’t have, production has remained minimal for years.

CATL, Contemporary Amperex Technology, comes into the picture. The Chinese firm, which is also the world’s largest battery manufacturer, eventually signed a $1.4 billion deal with Bolivia structured around this constraint. Rather than asking Bolivia to liberalize, CATL worked within the state-led framework. Under the agreement, the Bolivian state company YLB (Yacimientos de Litio Bolivianos)retains a 51% stake in the projects, ensuring formal ownership remains with the state. Meanwhile, CATL provides the investment and advanced ‘Direct Lithium Extraction’ (DLE) technology. It’s a perfect model that threads the needle between sovereignty and investment, showcasing flexibility that has characterized Chinese engagement across the region.

Chile, on the other hand, has more commercially feasible geology than Bolivia. This makes them the second-largest producer of lithium worldwide and a country where mining accounts for about 11% to 12% of GDP. The previous government under Gabriel Boric created a crucial state-led plan in 2023 – the National Lithium Strategy. The set of measures mandated Codelco, a state-owned Chilean mining company and the world’s largest copper producer, to hold majority ownership (50% + 1 share) in important projects. Now, under the new President, José Antonio Kast, the political environment has changed by 180 degrees. His 2026 administration is now moving toward deregulation and private-led models to attract more Western and Chinese capital. Nevertheless, the state-led Codelco-SQM partnership, a cooperation established under the previous administration, remains a cornerstone. It is too big to abandon since the Chilean state will receive the majority of the operating margin through taxes, royalties, and Codelco’s dividends. Still, operators like Rio Tinto are increasingly active as Chile balances state involvement with new market-friendly reforms.

The third and last player on the board is Argentina. Under President Milei, the country has gone the other direction entirely, opening aggressively to foreign investment through a new incentive regime called RIGI. Régimen de Incentivo para las Grandes Inversiones is a law that promotes large-scale, long-term investments exceeding $200 million by offering major corporate tax cuts from 35% to 25%, customs and foreign-exchange benefits, and 30-year benefits. The result has been something comparable to opening a dam. Firstly, Rio Tinto got a $2.5 billion company’s first commercial-scale lithium operation approved. Secondly, Chinese giant Zijin Mining committed $600 million to its Tres Quebradas (3Q) project, aiming to double its production capacity under the same tax protections. Last but not least, Chinese giant Ganfeng Lithium submitted a $3 billion proposal for its Pozuelos-Pastos Grandes (PPG) project to the RIGI, aiming for a massive 150,000-tonne annual capacity. Both Western and Chinese capital are competing in Argentina simultaneously, which arguably gives Buenos Aires more negotiating leverage than its neighbors.

The Processing Advantage

Contrary to popular beliefs, owning a lithium mine matters less than you might think. The real value and strategic leverage sit in what happens to the ore after it comes out of the ground.

Lithium extracted from brine or hard rock needs to be refined into lithium carbonate or lithium hydroxide before it’s useful for battery manufacturing. It is technically demanding, capital-intensive, and currently dominated by Chinese firms. The East Asian Power processes roughly 65% of global lithium, produces well over 80% of the world’s battery cells, and manufactures 56% of EVs. Even lithium mined in Chile or Argentina often travels to China for processing before re-entering global supply chains as a component in a finished battery.

This is not accidental. Over the past decade, Chinese companies, particularly Tianqi Lithium and Ganfeng Lithium, weren’t idle. They have systematically acquired stakes in upstream resources while simultaneously building out midstream processing capacity domestically. Between 2018 and 2024, Chinese companies invested over $16 billion in South American lithium projects alone. By 2023, Tianqi and Ganfeng collectively had access to nearly 40% of global lithium production through their South American operations. What everyone strives for? Vertical integration: control the mine, control the refinery, control the battery cell. This gives you the leverage at every stage of a supply chain that the entire energy transition relies on.

Because the metal under your feet is so important, it comes as no surprise that Bolivia has actually advocated for something that is comparable to how OPEC operates in oil – a lithium cartel among the three triangle countries. A proposal that is not irrational. Three neighbors controlling 60% of global reserves is a meaningful concentration; OPEC, for that matter, controls 80% of crude oil reserves. In practice, it’s unlikely to materialize, for several reasons. The three countries have fundamentally incompatible economic ideologies and with that three varying agendas. On one end, there is full state control, hybrid privatization being the middle, and on the other, there is Milei’s aggressive market opening, which adds even more friction when it comes to coordination. Lithium also lacks a standardized pricing mechanism, the way Crude and Brent oil have, which makes “cartel arithmetic” harder. Lastly, sodium-ion now acts as a price ceiling for lithium, offering a cheaper alternative for budget EVs and storage. Additionally, the 2022 price crash proved that if lithium costs spike, the market simply pivots to sodium or LFP, again undermining the leverage of a potential cartel. The price factor is also quite flexible as the market value of lithium dropped by about 90% from its all-time high in 2022. Furthermore, the rise of lithium recycling “urban mines” in the West allows for local supply recovery that bypasses South American monopolies. This just demonstrates that no one has permanent leverage.

Chancay

The most visible single expression of Chinese engagement in South America isn’t a mining deal, it’s a port.

In November 2024, President Xi Jinping joined Peruvian President Boluarte via video link to personally inaugurate the Chancay Port alongside Peruvian President Boluarte. The facility, built and majority-owned by COSCO Shipping at a cost of $3.5 billion, is the first deepwater port on South America’s Pacific coast capable of handling the world’s largest container vessels. Before Chancay, no such port existed on this coastline. Thus, ultra-large ships had no viable stop between Panama and the southern tip of the continent, which meant cargo from Pacific South America typically had to be transshipped through North American ports before reaching Asia.

Some details: Chancay cuts the transit time from the Peruvian coast to Shanghai from 35 days to 23. That’s an astronomical 12-day reduction. This shift translates into cost savings across everything Peru and its neighbors export, including copper, lithium, soybeans, shrimp, and fruit. In its first year of full operation, the port is projected to handle between 1 and 1.5 million TEUs, rising to 2.5 million at capacity.

Not only is the port built by a Chinese firm, but it’s also equipped with Chinese technology. The complex runs on Huawei 5G infrastructure, uses BYD electric trucks for autonomous container transport, operates fully automated cranes produced by ZPMC (Shanghai Zhenhua Heavy Industries), and tracks cargo via RFID throughout. It created long-term operational dependency that tends to deepen over time rather than diminish.

What makes Chancay genuinely significant beyond Peru is its connectivity. The port links via tunnel to the Pan-American Highway, meaning it functions as a gateway not just for Peru but for the entire western edge of South America. Bolivia, a landlocked country that will eventually need a Pacific export route for its lithium, has an obvious interest in using Chancay. Brazil has already expressed interest. It would help them in routing agricultural exports eastward by rail and then north through Peru. Ecuador too. They anticipate that cutting transit time will expand its perishable food exports to Asia significantly. And in April 2025, China launched a direct shipping lane from Guangzhou to Chancay, the first major direct route linking the two regions without North American stops.

What This Looks Like From the Chinese Side

It’s worth stepping back and understanding the internal logic of all of this and starting to connect the dots.

China’s 14th Five-Year Plan explicitly identifies lithium as a strategic resource. The country has committed to peaking carbon emissions before 2030 and achieving carbon neutrality by 2060, goals that require an enormous build-out of EVs and grid storage, which in turn require enormous quantities of lithium, cobalt, nickel, and copper. China doesn’t have enough of these materials domestically. It must import 70% of its lithium, 80% of its copper, and 95% of its cobalt. That is why their engagement in South America, at its core, is an industrial policy response to a genuine resource constraint.

Nevertheless, Chinese giants like CATL, BYD, and COSCO, apart from being backed by state policy, are real firms that answer to shareholders. Thus, their deals in Bolivia and Argentina make business sense in terms of an increase in revenue and general expansion. While many can say that these moves deepen China’s influence, they are, first and foremost, sound commercial investments that stand on their own merit.

The competition

But China isn’t the only one trying to gain a foothold in the region. They have to keep an eye on the EU and the USA, though neither really poses a threat right now. The former signed its long-negotiated trade deal with Mercosur in January 2026, after 25 years of stop-start negotiations. The EU is already Mercosur’s largest source of FDI at around $400 billion, so this agreement will only strengthen those ties by creating a free trade zone covering more than 700 million people. The latter has its own levers, including the Inflation Reduction Act’s critical minerals provisions, which create financial incentives for supply chains that don’t run through Chinese processing. But that’s the extent of it. Despite these frameworks, they have yet to exert any meaningful pressure on China’s regional lead.

The competition for South American resources is real, and it will intensify as the green transition accelerates. China has a significant head start, achieved by companies that moved early, adapted to local conditions, and built physical infrastructure that now shapes how the region connects to global markets. The focal point of this piece is still negotiating its future. Bolivia has yet to build a functioning lithium industry, Chile is shifting from state-led to private models, and Argentina has swung toward openness but could always swing back. None of these relationships is locked in permanently, but lithium, the quiet silvery metal sitting under those South American salt flats, is going to be contested for a long time.

Bibliography

Nem Singh, Jewellord. “How Latin America Can Harness the White Gold Rush.” Chatham House, March 2024. https://www.chathamhouse.org/publications/the-world-today/2024-02/how-latin-america-can-harness-white-gold-rush

Chekerdjievа, Christina. “Resource Nationalism in the Lithium Triangle: Analyzing the Investment Environment for China’s Projects in the Lithium Industry.” International Relations Review, May 2025. https://www.irreview.org/articles/2025/5/15/resource-nationalism-in-the-lithium-triangle-analyzing-the-investment-environment-for-chinas-projects-in-the-lithium-industry

Undisciplined Environments. “China’s Expanding Footprint in South America’s Lithium Triangle.” March 2025. https://undisciplinedenvironments.org/2025/03/11/chinas-expanding-footprint-in-south-americas-lithium-triangle/

AidData. “Chancay Port Opens as China’s Gateway to South America.” November 2024. https://www.aiddata.org/blog/chancay-port-opens-as-chinas-gateway-to-south-america

Center for Strategic and International Studies. “South America’s Lithium Triangle: Opportunities for the Biden Administration.” https://www.csis.org/analysis/south-americas-lithium-triangle-opportunities-biden-administration

Center for Strategic and International Studies. “The Geopolitics of Port Security in the Americas.” 2024. https://www.csis.org/analysis/geopolitics-port-security-americas

Washington Post. “China Opens Huge Port in Peru to Extend Its Reach in Latin America.” November 2024. https://www.washingtonpost.com/world/2024/11/14/china-peru-port-latin-america/

Asia Times. “China’s New Gateway into South America: The Port of Chancay.” November 2025. https://asiatimes.com/2025/11/chinas-new-gateway-into-south-america-the-port-of-chancay/

Wikipedia. “Port of Chancay.” https://en.wikipedia.org/wiki/Port_of_Chancay

U.S. Geological Survey. Mineral Commodity Summaries 2025: Lithium. January 2025. https://pubs.usgs.gov/periodicals/mcs2025/mcs2025-lithium.pdf

Mining.com. “Chile Mining Sector Faces Policy Test Under Kast Government.” March 11, 2026. https://www.mining.com/chile-mining-faces-policy-test-under-kast-government/

Shale24. “RIGI Map: Approved Projects and Those Still Pending for 2026.” January 4, 2026. https://www.shale24.com/en/oil-gas/rigi-map-approved-projects-and-those-still-pending-for-2026-n285

National Development and Reform Commission (NDRC), People’s Republic of China. The Outline of the 14th Five-Year Plan for Economic and Social Development (2021–2025) and Long-Range Objectives through the Year 2035. March 2022. https://en.ndrc.gov.cn/policies/202203/P020220315511326748336.pdf

0 Comments